Pia Sawhney

Insights

·

Moving Past 'Moving Fast'

For nearly two decades, Mark Zuckerberg’s motto “Move fast and break things” defined the ethos of the startup sphere. Founders were encouraged to be irreverent, impulsive, and stubborn to the point of intransigence. Rule-breaking was the key to victory: Nike wooed Michael Jordan by breaking the NBA rule stipulating that shoes had to be at least 51% white, while Zuckerberg, for his part, flouted the common sense that said advertising was the surest path to profitability. Steve Jobs, Bill Gates, and Larry Page and Sergey Brin all had reckless gambits of their own. The devil-may-care appeal of “move fast” was a natural fit in Northern California, where it dovetailed nicely with the entrepreneurial vision of a society loosed from East Coast starchiness and old-world conventions. Founders were rewarded for dreaming big and behaving outlandishly, even to excess; antisocial behavior was lauded as a key ingredient to progress.

It seems likely that the “move fast” ethos has contributed to the boom-and-bust nature of the venture capital market. While in the past the busts and booms would alternate, making the cycle more predictable to ride, today they overlap. The AI gold rush is coinciding with a market-wide contraction, as deal activity fell 75% percent in 2023 from last year. The mindsets that drive startup culture can be hard to pinpoint, but it’s clear that, too, they are evolving; in the wake of widespread layoffs and pandemic-fueled economic disruption, businesses now move more slowly and gingerly. At this stage, it’s time for the old models to retire the swift decision-making practices of the past and pay closer attention to business fundamentals in places overlooked by other investors.

In this moment, the value-laden ethos endemic to the Midwest, which might be described as “Move slow and make things,” is beginning to feel assured, prescient—even futuristic. Residents of the region have a reputation for being responsible and trustworthy, equally at home in a cornfield and in the HQ of a Fortune 500 company; in recent years, they’ve proved just as comfortable leveling up in scrappy five-person startups. Over the past two decades, the Old Midwest has undergone a metamorphosis, sprouting a panoply of irreverent independent bookshops and farm-to-table restaurants. That the region’s reputation for playing it safe endures is in no way a mark of a lack of entrepreneurial spirit, but rather of an appropriate wariness toward free-wheeling speculators. Driving up valuations, popular among coastal investors, can be heresy in American’s small towns. They know that not every risk means leaping off a cliff (where in Indiana do you even find a cliff?). Managing risk—understanding it, gauging it, traversing it—can be an incremental process.

So where does this ethos come from? Part of it is surely the chip on the shoulder from the “flyover states” barb, not to mention the innate thriftiness that comes from living in cities largely bereft of trigger-happy investors. But we think there’s something intangible to it as well, something that can’t be quantified. The Midwest, which stretches from the Corn Belt to the Rust Belt, is flush with industrial towns and family-owned farms that boomed and busted long before it was fashionable. Countless workers lost their livelihoods as manufacturing shifted overseas. They had to adapt to survive, bootstrapping businesses and making more of less (and less, and less). Midwestern stability signals not a lack of change but an abundance of it. It is a region ruggedized against upheaval and disaster, where risks can be met with equanimity.

It is said that venture capital is a long game, but “long” may not even begin to describe it. Legendary Union Square Ventures co-founder Fred Wilson remarked in 2021 that early-stage funds can often take 15-20 years to be fully liquidated. His essential insight (recognizing that startup culture can be unforgiving), is that investors (and entrepreneurs) who aspire to lead the field need ultimately to lead with patience.

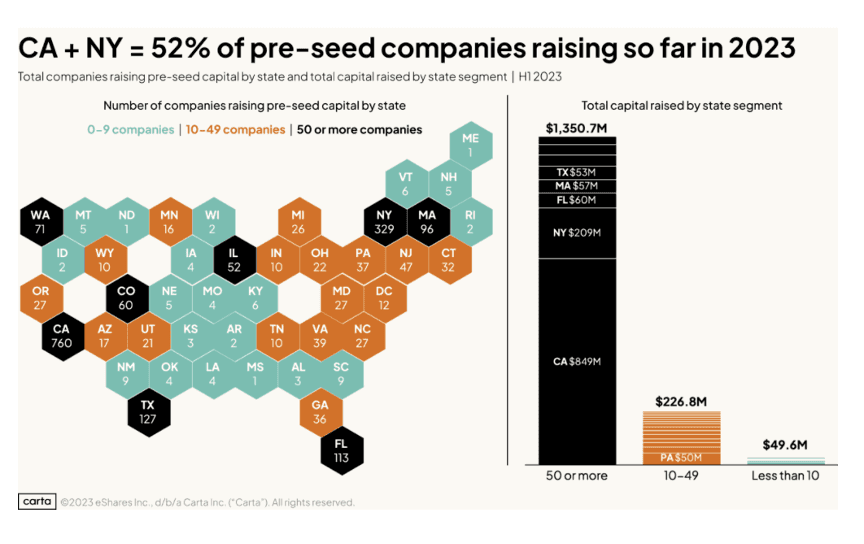

From our vantage point, with lower reserves in a capital-constrained environment, it’s the Midwestern ethos, captured especially by pre-seed and seed financing in the past several years, that is yielding early gains. Seed rounds, and especially SAFE instruments, are more popular than ever before. SAFEs increasingly extend beyond smaller cities, accounting for 80% of pre-seed invested capital on the coasts in 2023. Bridge rounds have also never been more significant; these, too, started in secondary cities before spreading to the coasts. And although California and New York raised $849M and $209M respectively in H1 2023, Pennsylvania, Michigan, Oregon, and Virginia, among others, all raised outsized pre-seed investments in the first half of the year. New Jersey, Connecticut, and Maryland followed closely behind, while Florida, Massachusetts, and Texas had more than 50 companies that raised pre-seed capital this year. Growth in the coming decade will reflect the rise of startups everywhere, as “friends and family” financing rounds morph into waves of larger, venture-scale investment. SAFE notes raised this year tended to have valuation caps, reflecting a more prudent order of angels getting involved in the startup game than ever before.

Source: CARTA “State of pre-seed fundraising Q2 2023” Report

Median check sizes are likewise relatively modest across the country, at least until companies raise their first $2.5M. Gone are the days of free-wheeling, “spray and pray” investing. Yet the venture capital market is not contracting so much as it is maturing—wising up while simultaneously expanding its horizons. Growth in secondary markets reflects this maturation. While “where you live” and “who you know” are hardly irrelevancies, they continue to yield ground to the far more important questions: why a given startup exists and how it distinguishes itself. In a leveled playing field, committed entrepreneurs in smaller markets are at an advantage—and while there's still a long way to go when it comes to distributing venture funding more equitably, the trend lines are at least pointing in the right direction.

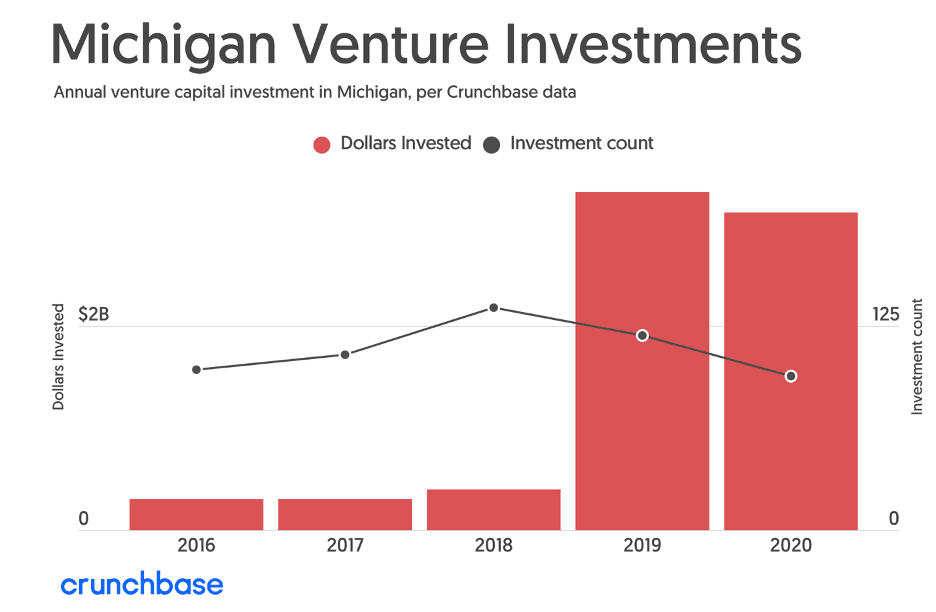

Between 2016 and 2020 alone, Michigan ranked first in the country for venture capital growth, with a nearly 900% jump from $300 million to $3.1 billion. Detroit and the areas around Ann Arbor experienced three times the investment in 2020 that they saw a year earlier; the region is now quietly home to five unicorn companies. If these success stories have yet to garner their fair share of national attention, that’s to be expected. The Midwestern ethos is about putting your head down, working hard, and not fretting over fleeting accolades.

We'll have more to say about the Midwestern tech sphere in future posts. In the meantime, watch this space.

Share: