Anthony Santaro

Insights

·

On Unicorns and Whales

Photo by Andrew Bain on Unsplash

In the eighteenth century, whale oil was the go-to light source for illuminating workers on night shifts, enabling a wave of unprecedented productivity for the British textile industry. While hardly a “technology” by today’s standards, whale oil was a great enabler of artificial light and held a promise not dissimilar to that of generative artificial intelligence in 2024 (as underpinned by semiconductors), or of the inchoate Internet in the 1990s (as underpinned by fiber optics).

Yet that hype often spelled disaster for fortune-seekers. Hyper-saturation of whale hunting grounds resulted in a brutally unforgiving market. 34.5% of whaling voyages failed to generate a positive return (for comparison, 32% of VC funds in the period from 1982-2006 had zero or net-negative IRR). It’s a lesson investors can draw from today, in the early days of the AI boom. In the whaling industry, the most outsized rewards tended to surface in unexpected places. While risk was inevitable, the riskiest move, paradoxically, was playing it safe, following the crowd.

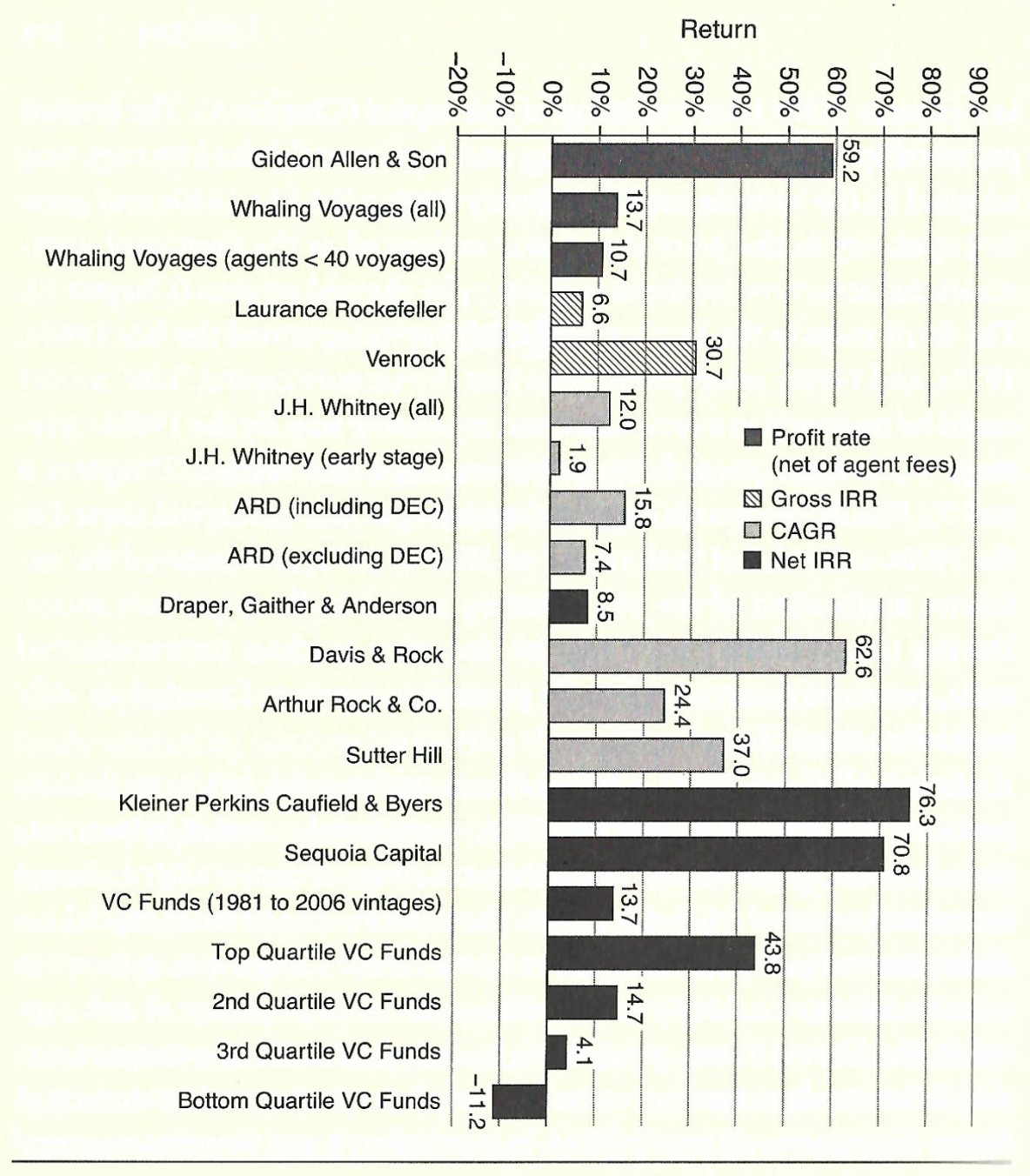

Absolute Performance: From Whaling Ventures to Modern VC Funds (from VC: An American History by Tom Nicholas). Note the uncanny equivalence between the profit rate (net of agent fees) of whaling voyages and the net IRR of VC funds (1981 to 2006 vintages).

Every revolutionary new technology needs a hub from which to spin out, and whale oil’s Silicon Valley was New England, initially in Nantucket and later in New Bedford, MA, where Ishmael begins his journey in Moby Dick. As Tom Nicholas argues in his book VC: An American History, whaling was the earliest iteration of venture capital, with whaling agents acting as the connective tissue between investor syndicates and ships.

Hired sailors (aka “whalemen”) held equity in voyages via the “lay” incentive system, while LPs stomached serious downside risk in pursuit of outsized returns. As with both venture capital and entrepreneurship in our era, whaling required tremendous discipline and was ill-suited to dilettantes and “tourist” investors. By the 1850s, the average whaling voyage took almost four years to complete, and many ships limped back to port with nothing to show for those years of toil (incidentally, roughly 70% of startups fail in their first five years of existence).

Nor were whaling voyages at all cheap. Nicholas cites a report that found that “the typical New Bedford whaling venture of the 1850s called for an investment of $20,000 to $30,000” — gargantuan sums for that era, especially compared to the cash outlay of virtually any other enterprise. Granted, New Bedford was well-equipped to finance these ventures: in 1853, the New York Times called it “probably the wealthiest place” in the country.

In the modern entrepreneurial lexicon, a “blue ocean” denotes a promising new vertical light on competition. Alas, nineteenth-century whalers quickly learned that the ocean wasn’t big or blue enough for all of them. Nicholas cites the research of one Eric Hilt, author of a paper entitled Investment and Diversification, who found that the high concentration of expeditions in particular whale-hunting grounds (like the North Pacific) significantly increased risk; these overfunded waters drew whalers in droves, many of whom would fall victim to what Nicholas dubs “herd-inducing cognitive biases,” or what our friend Seth Levine poetically described as “seven-year old soccer.”

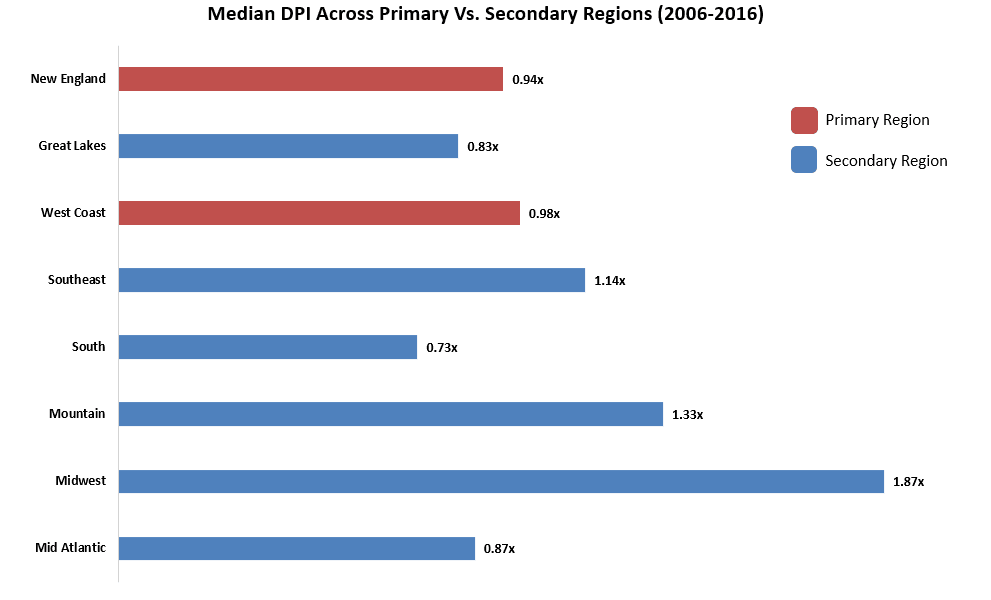

Today, VCs often suffer the same fate when following the herd. Much like with public equity investing, in VC there are considerable benefits to diversifying portfolios - geographically, demographically, and vertically. As the above graphic indicates, geographic diversification can come with the added benefit of superior DPI (Distributed to Paid-In Capital) as compared to more concentrated bets in primary markets like Silicon Valley. Past occurrence of whales (or unicorns) does not necessarily correspond to future returns. Diversification is not only a defensive measure, but one that lends itself to long tail outcomes.

In today’s post-ZIRP environment, startups must chart a course between the Scylla of taking too much money and the Charybdis of not taking enough. VCs, in turn, must determine which “hunting grounds” to direct their attention towards; should they obey convention, or strike out into untested waters? To be sure, there are still plenty of world-class companies being built in these legacy hubs, and Silicon Valley remains the early leader in the AI space (with New York right on its heels). Yet the data suggests superior returns can be found outside of these markets for thesis-driven investors willing to embrace uncertainty.

Share: